As predicted some years ago, demographic trends in Africa are now coming into play, including a burgeoning middle class and a rapidly growing youthful population. Parallel to this is the need for a variety of real estate options that is driving new economic activity. ‘More so given the commodity market slump, particularly that of the oil market, which had led to a shake-out in the industry,’ says Bronwyn Corbett, CEO of Grit Real Estate Income Group, previously known as Mara Delta Property Holdings.

‘The result is that while there are now fewer players in the market, a sense of sanity now prevails regarding cap rates and rentals, which have decreased – especially those in struggling resource-driven economies where we have seen some deep reversions in office rentals.’

While such a development may be encouraging, Corbett remains well grounded as to the challenges that remain, bearing in mind that each nation presents its own set of problems. ‘Generally speaking though, currency fluctuation and the ability to repatriate funds remain as barriers to investment and development. For our group, currency risk is minimal because a large part of our income is derived in US dollars or euros. In a select number of instances, usually smaller retail tenants, a lease contract will be in local currency and the cash flow derived from that is directed at settling in-country expenses.

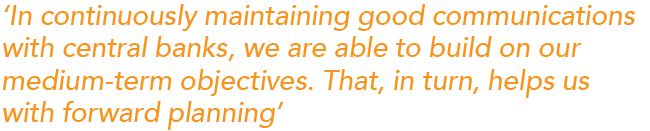

‘In the case of repatriation of funding, which many perceive as risky, our experience is that if you have the patience, guidance and perseverance to work through regulatory processes, it will stand you in good stead,’ says Corbett. ‘And in continuously maintaining good communications with central banks, we are able to build on our medium-term objectives. That, in turn, helps us with forward planning.’

Mozambique presents such a case, from both a repatriation perspective and land-use by citizens. Corbett explains that despite a restriction on repatriation of US dollars from Mozambique, due to it defaulting on IMF repayments, her company has still been able to transfer funds successfully. ‘We provide the Central Bank with upfront planned withdrawals and the necessary supporting documentation. It is when foreign investors attempt to expedite the process that trouble is encountered,’ she says.

Mozambique also applies the rule of Direito do Uso e Aproveitamento da Terra (DUAT), which allows citizens to use and benefit from land but not sell or mortgage it, except in the case of the building of any infrastructure. ‘The ability to identify the rightfully registered beneficiary of a DUAT over a specific land parcel, as well as the legal system enforcing the leasehold contract, has given developers enough security to negotiate and develop infrastructure and real estate assets in key nodes, resulting in an infrastructure boom in that country,’ says Corbett.

Working and complying with regulations has always been a bit tricky in Africa and it’s no different within the real estate sector. Consider that, with 54 different investment jurisdictions, sifting through a multitude of tax and treaty regimes can be disheartening let alone confusing and time-consuming. While investors may be doing the sensible thing in connecting with informed and reputable local counterparties and the appointment of local tax and legal experts, Corbett points out it requires allowing and trusting them to execute on their mandate.

New investors can also be confounded by not just geopolitical environments but the macro- and micro-economic risks of each territory or region. ‘Among the reasons that Grit has built a successful track record in Africa is because we transact with large international companies in hard currency leases, and we have spent enough time inland peeling back the layers of real estate investment environments to ensure a comprehensive understanding of the influential factors at work.

‘This is a critical strategy that also relates to understanding what our investor requirements are and how they measure the performance of their investment, be that in terms of total return growth, distribution growth or net asset value growth. Obviously such investment is dependent on country risk mitigators such as location, size of asset, quality of tenants, duration of leases, occupancy rates, current and future competition, and operational costs.’

Corbett confirms that real estate in Africa has for years lagged equities as an asset class. ‘The market is only now starting to scratch the surface with more sophisticated analytical needs. Different markets measure relative performance differently. In South Africa, the promulgation of real estate investment trust [REIT] status has catapulted listed property into one of the best-performing asset classes over a number of years. This was stimulated by record low interest rates and a market focused on distribution yields.’

Currently there are only four countries in Africa with REIT regimes but similar structures are being implemented across the continent. ‘We expect the tax benefits associated with these structures to stimulate significant investments into real estate over time, especially given there is a strong correlation between the investment mandates of pension fund investment schemes and the investment characteristics of listed real estate,’ says Corbett.

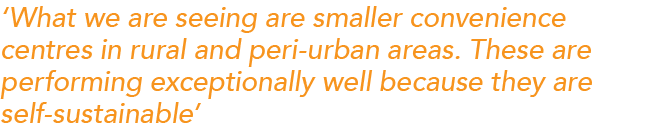

Property investors are also becoming more strategic in their planning, largely as a result of movements towards urbanisation and associated infrastructure needs. ‘Gone are the days where super-regional centres are developed. What we are seeing are smaller convenience centres located in rural and peri-urban areas. These are performing exceptionally well because invariably they are self-sustainable as far as electricity generation and potable water is concerned, allowing for uninterrupted trade despite infrastructure challenges,’ says Corbett.

This, however, means that while green-built initiatives are welcomed, there has to be a competitive advantage over traditional methods. ‘In our experience, having solar energy and harvesting grey water in our super-convenience centres is working well. A landlord is able to offset savings on electricity and water against rental rates, and long-term there is the potential to feed excess capacity into the grid for the benefit of surrounding communities.’

Usually sited along taxi routes and in proximity to towns, these centres also cater to the growing popularity of live-work-play environments within the same precincts, which supports nodal development that includes entertainment and leisure activities, education and healthcare. ‘Developers, therefore, often need to take care of issues beyond their own fence line. This might include secondary roads, water, power and sanitation infrastructure.’

Corbett explains that such nodal development has given rise to new towns that have the potential to develop into cities as critical mass gains momentum. However, while the DNA of nodal development may lie in supporting community needs, doing so comes with a cost premium and therefore can be a potential differentiator for the developer in whether to invest or not.

‘This is why public-private partnerships [PPPs] are important – those that also include logistics solutions such as storage, rail, air and sea developments. History has shown that PPPs provide a win-win solution for governments, landlords and large corporations with the added advantage of creating other real estate opportunities,’ says Corbett.

This is certainly true in East Africa, where, for example, the growth of professional services and even SMEs has resulted in not just the area developing strong regional hubs but also some relatively high rental returns on the back of current limited availability of office space. ‘It remains, however, that Africa – excluding South Africa – is experiencing “buyer’s market” conditions,’ she says.

What real estate investors must bear in mind in Africa though is that property ownership alone is not quite enough, according to Corbett.

‘Having physical assets is only one part of the solution. Economic growth in Africa can only work by using such investment to stimulate employment creation and specialist skills development.’