What is the definition of being middle class in Africa? The true size of this burgeoning social tier is hard to pin down in its complexity. ‘Typically, the emergence of a “consumer class” helps to propel growth to the next level,’ Razia Khan, chief economist for Africa at Standard Chartered Bank, wrote in an opinion piece for How We Made It In Africa earlier this year.

‘With rising disposable incomes, there are opportunities to consume an even wider array of products. Demand grows, spending grows, businesses prosper, employment grows, the middle class grows, economies grow… It’s an important virtuous cycle.’ But who is this new consumer class?

A 2011 report by the African Development Bank (AfDB) came to the – now controversial – conclusion that in 2010 every third person in Africa was part of the middle class. This translated to 34.3% of the continent’s population, a total of 326 million people.

A 2011 report by the African Development Bank (AfDB) came to the – now controversial – conclusion that in 2010 every third person in Africa was part of the middle class. This translated to 34.3% of the continent’s population, a total of 326 million people.

According to these figures, Africa’s middle class had thrived over the previous two decades – from 26.2% (about 115 million people) in 1980, 27% (157 million) in 1990 and 27.2% (204 million) in 2000.

A wave of Afro-optimism followed, with high expectations of the positive socio-economic and political impact this growing class would potentially have. Numerous media headlines reflect this excitement. ‘The Rise and Rise of the African Middle Class’; ‘The Lion Kings’; and ‘Africa’s Burgeoning Middle Class Brings Hope to a Continent’…

However, the AfDB definition is extremely broad, thereby overestimating its size and prowess. Per definition, the study considers anyone with a per capita daily consumption of US$2 to US$20 (in terms of purchasing power parity) as a member of the middle class. About 60% of those belong to the so-called ‘floating middle class’ (living on US$2 to US$4 per day), which renders them ‘unstable’ and ‘largely vulnerable to slipping back into poverty’.

This group, which might be better classified as ‘non-poor’ instead of being included in the middle class, was duly omitted in a 2015 study by the Pew Research Centre. According to the US-based firm, only those with a daily per capita income of US$10 to US$20 qualify as middle-income earners. This would make a mere 6% of the continent’s population middle class – a size that only marginally increased in the decade leading up to 2011.

During the same period, poverty rates in sub-Saharan Africa dropped significantly but the majority of households that crossed the poverty line only made it into the low-income group, unable to move above the US$10 middle-income threshold.

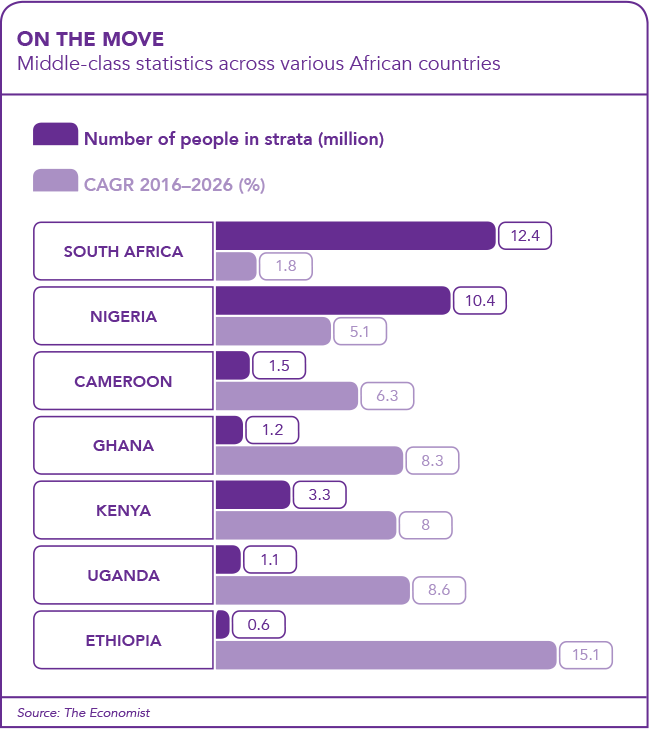

Adding to this fluctuating picture, a 2014 Standard Bank survey of 11 countries in sub-Saharan Africa defined middle-class households as having an annual income of at least US$5 500. Consequently, just 14% of respondents were considered middle class, with Angola and Nigeria showing the fastest growth.

Whatever the definition, a middle-class existence doesn’t automatically start at a monetary threshold. ‘A low wage is better than none at all but those living on US$10 to US$20 a day are hardly sipping sangrias at sunset,’ writes a journalist in the Economist. ‘For most of them, life is still tough.’

As a rule of thumb, being middle class implies discretionary expenditure. So a member of the middle class should be able to buy all the basic necessities and still have money left to spend on non-essentials – such as a sangria sundowner and more expensive treats.

According to Khan, ‘middle class’ typically refers to households that spend a minimum of 50% of their income on goods and services beyond mere food and basic necessities. ‘The ability to earn a steady, regular income is now increasingly recognised as the one factor that distinguishes those living in poverty from those able to emerge as middle income,’ she says.

For many, however, the wolf looms at the door. ‘It’s unfortunately true that the average middle class South African is only two pay cheques away from financial hardship,’ says Jannie Rossouw, head of the School of Economic and Business Sciences at Johannesburg’s Witwatersrand University.

‘The middle class in many countries in Africa is “first generation” and therefore not used to the challenges and dangers that a middle-class existence faces. They have no experience, for instance, of the devastating affect of a middle-class breadwinner being retrenched and without a job for a prolonged period of time.’

He says that it’s a long reach from the lower to the upper middle class. An upper middle-class family is nearly seven times better off than a lower middle-class family. Writing in a co-authored article on the challenges in becoming and remaining middle class, Rossouw says: ‘With reaching middle class status comes new challenges. Middle-class status results in a particular lifestyle. A household equipped with gadgets and equipment using electricity (fridges, freezers, TV and the like). A motor vehicle. A better house and better schools for the children.

‘Simply put, in a middle-class existence, expenditure follows income. More middle-class trimmings follow a middle-class existence. What was good enough before is no longer good enough.

‘Middle-class people borrow money to purchase things associated with middle-class existence. There are many examples of middle-class people living above their means. One is expensive and flashy cars. The neighbours must see that middle class has arrived.’

A way of stabilising the middle class is to encourage households to live within their means and also to save and make provisions for retirement, in order to retain their lifestyle.

‘People – not only the middle class but particularly the middle class – must be educated about money, expenditure, taxation and savings,’ says Rossouw.

Policymakers can assist in this through financial education in school curriculums and through tax legislation. In 2016, for instance, South Africa’s Tax Law Amendment Act harmonised the tax treatment of retirement funds in a bid to help people save for their retirement. It encourages income tax-free retirement investments to a certain limit and on the condition that no more than one-third is paid out as a lump sum and the rest is used to provide a monthly annuity upon retirement.

However, the most important boost for the middle class will be sustained economic growth and foreign direct investment.

‘Economic growth protects the incomes of those already employed,’ says Rossouw. ‘It also creates employment opportunities for new entrants to the labour force and – through employment – to the middle class.’

While some multinationals have cut back their investment on the continent, blaming the slow growth and small scale of Africa’s middle class, other global players are demonstrating confidence.

Volkswagen already has a strong presence in South Africa, Nigeria and Kenya, with plans to launch an integrated mobility concept in Rwanda at the end of this year. The novel concept is based on app-based mobility solutions such as car sharing and ride hailing.

Volkswagen South Africa chairman and MD Thomas Schäfer says: ‘Africa is still one of the blank spots on the Volkswagen map. There is enormous potential in the region to meet the mobility needs of a burgeoning middle class.’

Another growth area is hospitality. Hotel investment throughout sub-Saharan Africa is set to reach US$1.7 billion in 2017 and a further US$1.9 billion in 2018, according to real estate experts Jones Lang LaSalle.

Marriott (owner of luxury brands Sheraton and Ritz Carlton) said in a statement: ‘Africa is particularly important to Marriott International’s expansion strategy because of the continent’s rapid economic growth, expanding middle class and youth population.’

The sheer headcount of the continent’s rapidly expanding youth population will make Africa interesting for investors. According to the UN, by 2025 Africa will be home to three megacities (at least 10 million people) – Lagos, Kinshasa and Cairo – and 12 cities with more than 5 million inhabitants.

‘Positive demographics drive growth exponentially,’ says Khan. ‘Although formal-sector job creation remains a challenge, other things being equal, this demographic profile should boost Africa’s growth – driving up consumption and asset prices, as well as creating a greater pool of pension savings that can be invested in the region.’ And this has the potential to kick-start the virtuous cycle of the new consumer class.

In tandem, however, African governments and decision-makers should strive to narrow the inequality gap between extreme poverty and the very wealthy. This would further strengthen the burgeoning middle class, which can only truly flourish when the rest of the population is also in a healthy state.